(Bloomberg) — Nvidia Corp. assured investors that its new product lineup will continue to fuel an artificial intelligence-driven growth run, while also signaling that the rush to get chips out the door is proving costlier than expected.

Most Read from Bloomberg

Listen to the Bloomberg Daybreak Europe podcast on Apple, Spotify or anywhere you listen.

Speaking after the release of quarterly results, Chief Executive Officer Jensen Huang said that Nvidia’s highly anticipated Blackwell products will ship this quarter amid “very strong” demand. But the production and engineering costs of the chips will weigh on profit margins, and Nvidia’s sales forecast for the current period didn’t match some of Wall Street’s more optimistic projections.

That brought a tepid reaction from investors, who had bid up Nvidia shares almost 200% this year heading into the earnings report. After that dizzying rally, which turned the chipmaker into the world’s most valuable company, anything but a blowout quarter was bound to be a disappointment.

The shares fell as much as 3.6% on Thursday before rebounding by the afternoon. They closed up 0.5% at $146.67.

Nvidia predicted fiscal fourth-quarter sales of about $37.5 billion. While the average analyst estimate was $37.1 billion, projections ranged as high as $41 billion.

“The guidance seems to show lower growth, but this may be Nvidia being conservative,” said Alvin Nguyen, an analyst at Forrester Research Inc. “Short term, there is no worry about AI demand. Nvidia is doing everything they should be doing.”

The company’s biggest moneymaker is its accelerator chip, which helps develop artificial intelligence models by bombarding them with data. Since OpenAI’s ChatGPT chatbot debuted in 2022, a frenzy of AI services has created insatiable demand for the product.

All About Nvidia Chips, AI Hype and What Lies Ahead: QuickTake

Wall Street has been closely watching the launch of Blackwell, the latest entry in that category, which is faster and has an improved ability to link up with other semiconductors. Manufacturing challenges have slowed the rollout, and Nvidia warned again of supply constraints on Wednesday. Demand for the products is expected to exceed supply for several quarters.

“Critical questions around Blackwell’s production ramp and customer concentration remain key concerns,” Emarketer analyst Jacob Bourne said in a note. “There’s little room for execution missteps in 2025.”

Huang said that Blackwell is now in “full production,” and there’s still an appetite for Hopper, the previous design. “Blackwell is now in the hands of all of our major partners,” he said during the conference call.

But the switch to Blackwell has taken a toll on profitability. The company’s gross margin, which measures the percentage of sales remaining after deducting the cost of production, will dip to as low as 73% this quarter from 75% in the previous period. The figure is expected to rebound when the new products reach larger-scale production, and the economics are more favorable.

When asked whether Nvidia’s gross margin could be back in the mid-70s by the middle of next year, Chief Financial Officer Colette Kress said that’s a reasonable assumption. Nvidia remains far above its peers in this category: Its nearest rival, Advanced Micro Devices Inc., has a gross margin that’s 20 percentage points narrower. Intel Corp.’s isn’t even half of Nvidia’s total.

Nvidia’s growth over the past two years has been staggering. Its sales are poised to double for a second year in a row, and it now notches more money in profit than it used to generate in total revenue.

Nvidia’s revenue rose 94% to $35.1 billion in the fiscal third quarter, which ended Oct. 27. Excluding certain items, profit was 81 cents a share. Analysts had predicted sales of about $33.25 billion and earnings of 74 cents a share.

Nvidia’s biggest division, the data center unit, saw revenue double from a year earlier to $30.8 billion. That beat Wall Street estimates.

But networking revenue within that unit declined sequentially, and the business is more dependent than ever on a small group of customers: cloud service providers. That cohort, which includes companies such as Microsoft Corp. and Amazon.com Inc.’s AWS, accounted for 50% of data center revenue, up from 45% in the prior period.

Investors want that number to go down, to show that the use of AI is spreading across the economy.

Other recent earnings reports have given strong signals for AI. Nvidia customers, including Microsoft, Amazon and Meta Platforms Inc., have reaffirmed their commitment to spend heavily on AI infrastructure.

WATCH: Nvidia’s Surprising AI Origin Story

Nvidia has only missed analysts’ estimates on quarterly revenue once in the past five years. And it has exceeded expectations by as much as 20% in recent periods, creating a high bar for its performance.

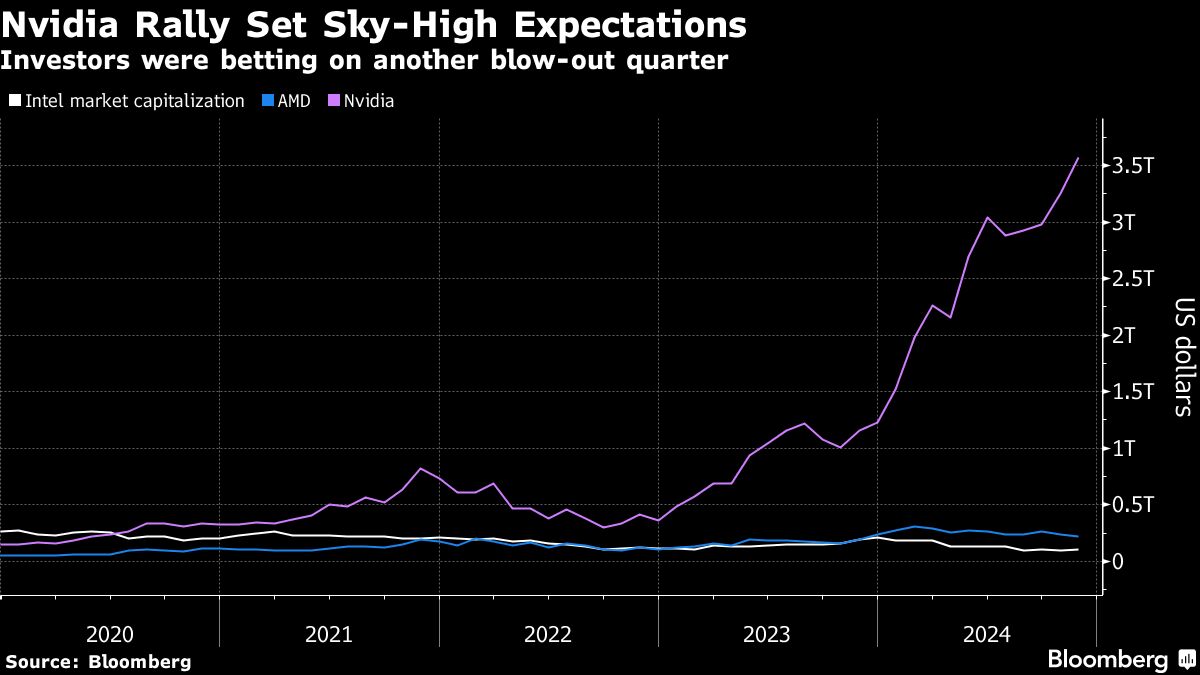

Its data center division alone now has more revenue than rivals Intel and AMD have in total, combined. Net income this year is on course to exceed revenue at Intel, a business that was the chip industry’s biggest company for decades.

Nvidia made its name by selling graphics processors, but discovered that the technology also has applications for AI. Its chips help software models during the training process, when they learn to recognize and respond to real-world inputs. Nvidia’s components are also used in systems that then run the software, a stage known as inference, and help power services such as ChatGPT.

The Santa Clara, California-based company has rapidly expanded its product lineup to include networking, software and services, as well as fully built-out computer systems. Huang is traveling the world lobbying for a broader adoption of his technology and trying to spread its use by corporations and government agencies.

“The age of AI is upon us and it’s large and diverse,” Huang said.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Source link